Sole trader or landlord? Stay compliant with our MTD for Income Tax software:

free, simple and built into your account.

500,000+

Business owners bank with Starling

Making Tax Digital: all sorted, all free.

From April 2026, sole traders and landlords in the UK with a qualifying income of over £50,000 in the last tax year must digitally report their income tax and expenses to HMRC (is that me?). Luckily, we’ve got just the tool to help.

MTD for Income Tax software.

Life’s too short for extra logins.

Our MTD tool is part of your sole trader account.

You’ll find it in Accounting Essentials, included for free with your sole trader account.

Submit to HMRC directly from your account.

Quarterly updates: send them to HMRC at the click of a button. End-of-year declarations coming soon.

Banking that’s good for the sole.

Instant notifications, spending insights, 24/7 support and a whole lot more. It’s all part of our free sole trader account.

HMRC-recognised tool.

Quarterly submissions? Tick.

Income and expenses tallied as you go.

Categories assigned to business and property expenses, which you can review and change.

Automatic invoice and transaction matching.

Add transactions from outside Starling.

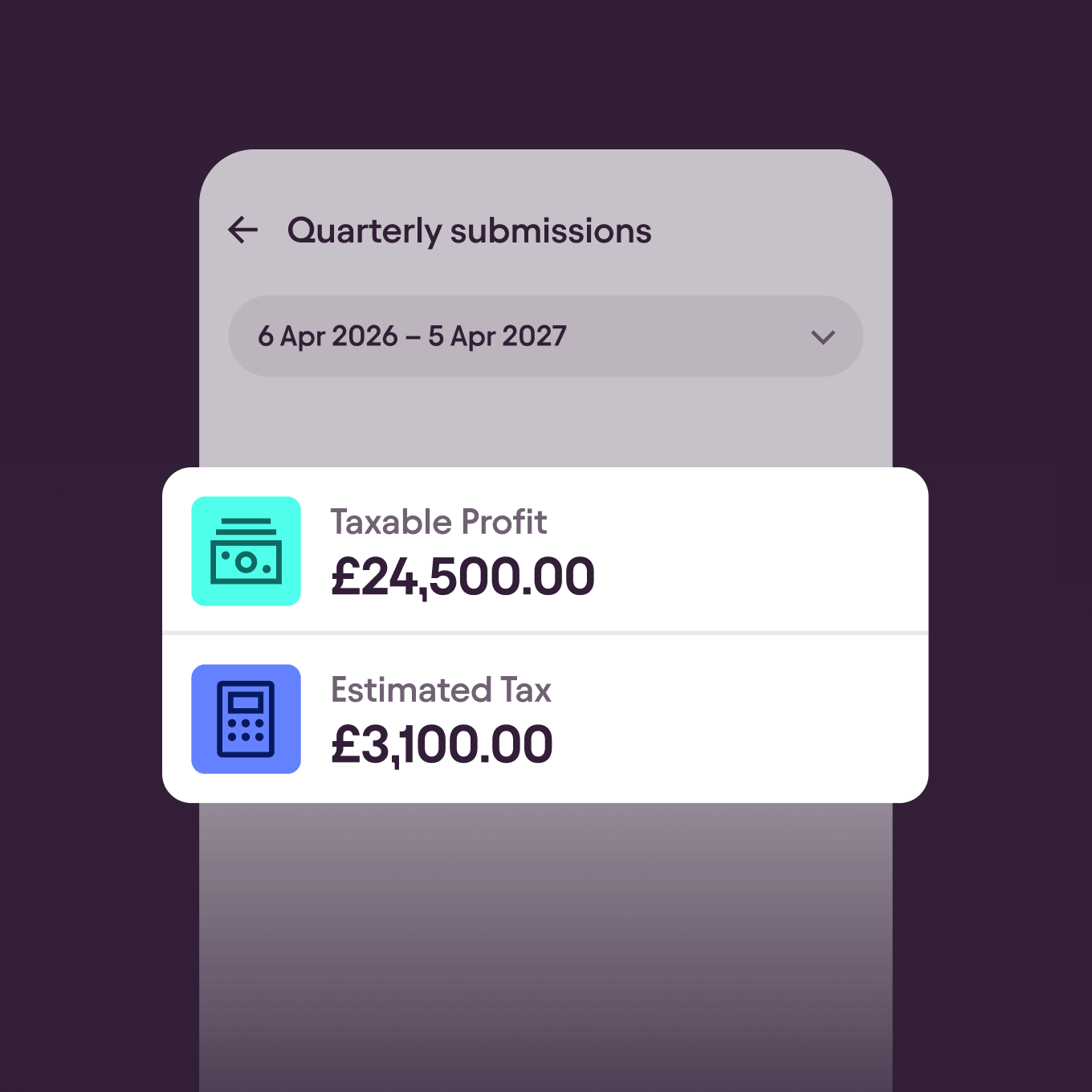

See your taxable profit, owed tax and submit quarterly updates with a click.

We’ve got your back.

Never miss a tax deadline.

With reminders, checklists and timelines – as well as human support available 24/7 – we’ll keep you in the loop, and help you stay compliant.

Log in to Online Banking and head to the Accounting tab to find our MTD software. Or, if you don’t have an account yet, apply for a sole trader account to get started.

Log in to Online Banking to explore our MTD software.

Tax made a little less taxing.

Set aside money as you go, with real-time estimates and a dedicated Space for your owed tax.

See how much tax you owe.

Every time you receive or spend money, we’ll update your taxable profit and the amount you owe in tax ‘as it stands’.

Set aside money with a Space.

You can put the money you need for tax into a separate Space as you go. That way you can’t accidentally spend money you don’t really have.

Accounting Plus

Need to do VAT returns?

Submit VAT returns directly by upgrading to Accounting Plus.

What’s included:

Submit VAT returns directly to HMRC.

Stay on top of tax with automated calculations.

Coming Soon: More features and tools to help you save time and focus on your business.

Apply for a sole trader account, then upgrade to Accounting Plus for just £7 a month until April 2027, then £14 a month. Cancel anytime.

50% off until April 2027

“It’s so simple and straightforward to use. I’m not an accountant – I just want things to be clear and not overwhelming. It ticks all the boxes.”

Natasha Swan Ceramics

Starling Accounting Customer & Business Owner

The Making Tax Digital Journey.

Making Tax Digital already covers VAT and, from April 2026, will extend to income tax self-assessment. Here’s a timeline of the government’s implementation plan.

April 2022

MTD for VAT applies to all VAT-registered businesses.

April 2026

Self employed and property businesses earning over £50k will need to submit income tax self assessment returns through MTD for Income Tax.

April 2027

MTD for Income Tax will apply to self employed and property businesses earning over £30k.

April 2028

MTD for Income Tax will apply to self employed and property businesses earning over £20k.

Apply for a sole trader account today.

No monthly fees. 24/7 support. Industry-leading security features.