Everything you need to know about children’s bank accounts

Everything you need to know about children’s bank accounts

When it comes to looking after your child, looking after their money and teaching them how to save and spend safely is key. Here, we run through what you need to know about children’s bank accounts, as well as prepaid cards and Under 16s, our free debit card for kids.

What are children’s bank accounts?

Bank accounts for children or teenagers are similar to adult bank accounts, but usually come with certain restrictions. For example, a child bank account won’t have an overdraft and may have additional security features, controlled by the adult.

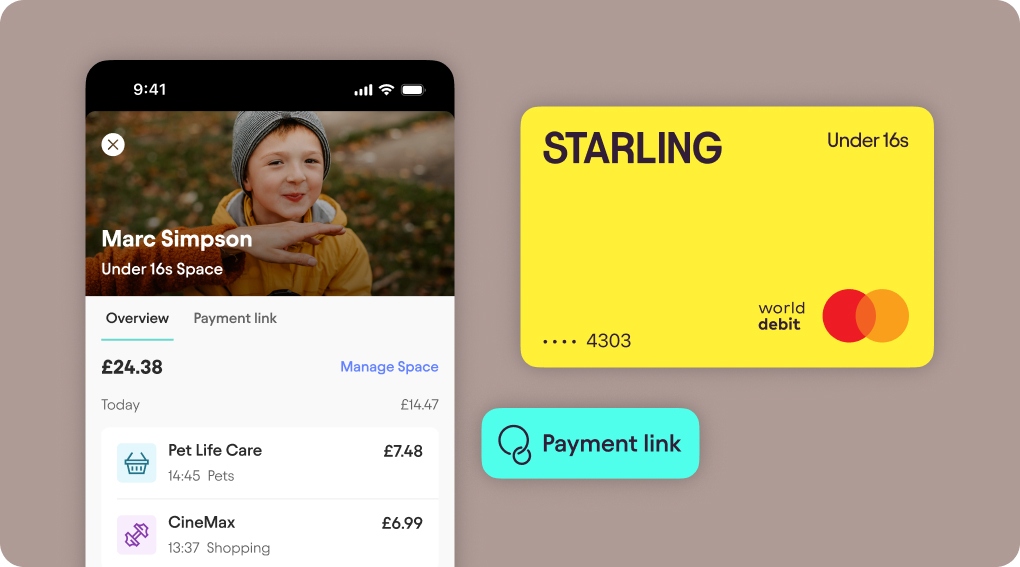

Under 16s is a Space in the adult’s bank account with a debit card attached. The adult can top up the debit card from their Starling app and any money added will be protected through the Financial Services Compensation Scheme (FSCS) up to £120,000. Under 16s is a free debit card and app. There are no fees for withdrawing cash or topping up the card and the Space includes more features than a child bank account usually would.

What alternatives are there to children’s bank accounts?

Another alternative to children’s bank accounts are prepaid cards, which usually include an app that can be controlled by adults. There are a number of differences between a child bank account and a prepaid card. First off, a company that offers a prepaid card usually isn’t a bank, meaning that your money won’t be covered by the FSCS directly, but may be covered through a third-party. They also tend to have fees for withdrawing cash and topping up the card, plus a monthly fee.

One of the advantages of a prepaid card is that it offers adults more control than child bank accounts, giving them the ability to set spending limits or add rewards if their child has completed their chores.

How do children’s bank accounts work?

People under 18 can use their bank account in similar ways to people over 18. From a child bank account, you can:

make and receive payments

withdraw cash

make purchases in shops or online

set up Direct Debits or standing orders

The main thing children can’t do is borrow money - children’s bank accounts don’t have overdrafts.

With Under 16s, an adult can give a card to children aged 6-15 to make purchases. The account owner who set up the Space also has the option to block certain payments, for example, transactions made online or cash withdrawals. All Under 16s cards are blocked for transactions made at gambling or betting merchants. Every time a payment is made on the card, the account owner/s will receive a real-time notification detailing the merchant and the amount to give them insight into their child’s spending.

How old does a child have to be to have a child bank account?

Usually, your child has to be at least 11 years old to open a child account. Some banks have a higher age limit of 16. You may also find that additional features are made available once your child turns 16. Prepaid cards are usually available to children aged 8 and above.

Under 16s is available for children aged 6-15. Once your child turns 16, they’ll have the option to apply for a young persons account, similar to an adult personal account but without certain features like an overdraft facility.

What are the benefits of children’s bank accounts?

Benefits of setting up a child’s bank account include:

independent money management, enabling your child to check their balance and learn more about how to save and budget

no overdraft facility, meaning that your child can only spend the money in their account and can’t get into debt

daily withdrawal limit, depending on which bank provides the child account

interest earned, depending on which children’s bank account you choose

Under 16s enables children to learn about spending money and keeps adults in the loop through real-time notifications. Like a child bank account, there is no overdraft facility for Under 16s - children can only spend what an adult adds to the card. There are no fees for topping up the card or withdrawing cash and adults can block certain types of payments, for example, online transactions.

How should I choose a bank account for my child?

Do your research before choosing which bank account is best for your child. Things to check include:

age limits

fees

extra features

ability to download an app or do online banking

reviews on the bank’s customer service

Opening a bank account for a child

For children under 16, the bank account will need to be opened by their parent, guardian or grandparent either in a branch or online. For those over 16, they can set up the account themselves, without parental consent.

How to open a bank account for a child

The account set-up varies from bank to bank. Some banks allow you to set up an account online or through the mobile banking app. Others require you to visit a branch to complete the application process.

What do I need to open a child bank account?

To open a children’s current account, you’ll need:

your child’s passport, birth certificate or provisional driving licence as proof of ID

your own proof of ID and your proof of your address, for example, an energy bill or council tax bill

After my child turns 18, what happens to their bank account?

Normally, the child’s bank account will upgrade to an adult’s current account automatically. But you may need to request for this change to be made.

With Starling, your child can apply for their own Starling bank account by downloading the app. Once they have their adult account, you have the option to transfer money from their Under 16s Space to this.