Saving

Cash ISA allowances are changing.

By Charlotte Lorimer

Good with money

“It’s all about taking things one step at a time,” says Nicholas Hill, money expert at MoneyHelper. “But remember that the sooner you start, the sooner you’ll feel in control.”

Sometimes, a problem shared is a problem halved. If you’re worried about money or how to manage your bills or debt, talking to a trusted friend, family member, partner or a recognised financial advice service could relieve anxiety and ultimately lead to the support you need.

“You don’t have to feel isolated,” says Nicholas. “There is free, independent guidance available through the MoneyHelper website, where you can learn more about money or speak to one of our experts.”

“I’d always encourage people, particularly those on a lower income, to use a benefits calculator and check whether they’re getting all the state benefits they’re entitled to,” says Nicholas.

If you find you’re entitled to a benefit you’re not currently receiving and decide to make an application, you might want to ask how long it usually takes for it to be reviewed. That way, you’ll know when you might have more money coming in each month.

Opening your banking app or gathering together old statements is going to feel overwhelming. But if you don’t know where you’re at or what you’re spending most on, you’re going to struggle to change how you manage your money – and how you feel about it.

As you look through, remember that the ultimate goal is making a budget that can give you some guardrails for your spending. You might find it helpful to open our Budget Planner, which is free for anyone to use.

The categories in the Budget Planner can help you understand what to look for and work out from your statements: How much money do you have coming in each month? What do you need for your rent or mortgage, council tax and household bills? What do you spend on food and transport to and from work?

“It’s also important to look through credit card statements and the tax code on your payslip to make sure that HMRC are taking the right amount of tax,” says Elizabeth Webb, a Fairstone Chartered financial planner.

“Budgeting is one of the cornerstones to managing your money. It can put you in the driving seat, so you can choose where and how to spend your money,” says Nicholas.

Once you know how much money you have coming in after tax (including benefits) and what your monthly costs are, set targets for your spending with a budget.

Some people follow the 50/30/20 budgeting rule and allocate 50% of their income for essentials (such as rent, food and household bills), 30% for things they want or like to do and 20% for savings and paying off any debt. These percentages won’t be realistic for many people, but some may find the general principle of allocating set proportions to different types of spending helpful.

Others find it more helpful to plan their spending with more detailed categories, such as rent, utility bills, family, groceries, fitness, eating out, savings and debt repayments. If you bank with Starling, you can use our Spending Intelligence feature to review your spending by asking questions such as ‘How much did I spend in supermarkets last month?’ or ‘What have I spent on my pets this year?’.

Whatever budgeting method you choose, you may find it helpful to separate money for different purposes into different places. “Set up direct debits to somewhere else as soon as your money comes in,” says Elizabeth.

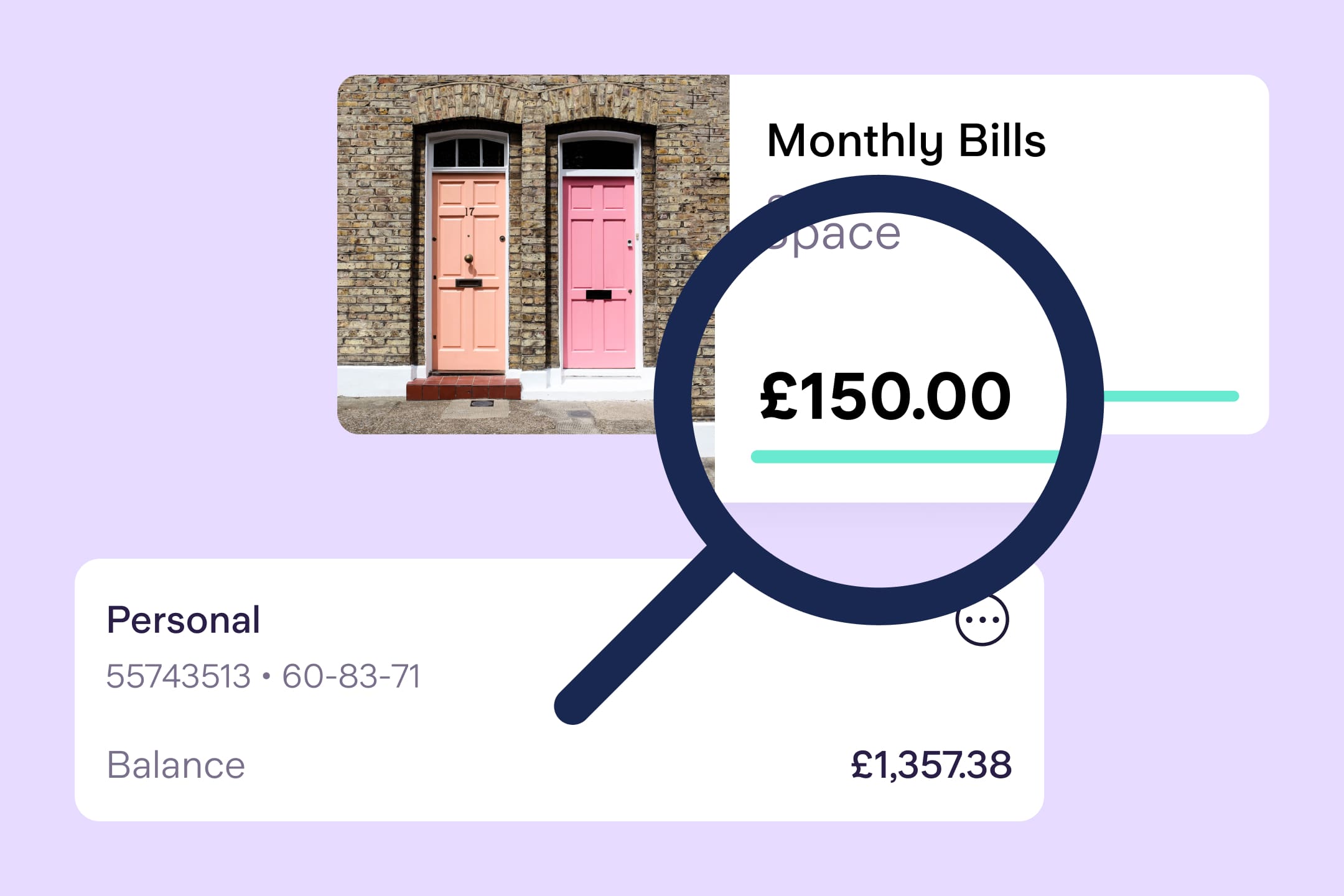

If you’re a Starling customer, you could create different Spaces within your app to keep your money for bills or groceries separate from your main balance – and set up automatic transfers so you don’t accidentally dip into the money you need for your rent or electricity bill.

You can even pay your rent or electricity bill from a particular Space with our Bills Manager feature – simply connect standing orders or Direct Debits to your ‘Bills’ Space.

Once you’ve made a budget, you’ll find it much easier to see where you might be able to save money. “Pick one monthly outgoing and choose to reduce or remove it,” says Elizabeth.

It’s worth paying attention to:

Subscriptions (some can be reduced by moving to a shared or family plan)

Memberships (gym, clubs, cultural organisations)

Broadband bill (if coming up for renewal)

Phone bill (if you’re out of contract, moving to SIM only might cut your bill)

Insurance (check you have the right cover for your needs)

Nicholas also recommends leaving online purchases in your basket for 24 hours before deciding on whether you really want to go ahead.

If debt is your biggest money worry, you can use MoneyHelper’s free debt advice locator. “There are government schemes designed to help,” says Nicholas.

“For example, the ‘Breathing Space’ scheme could provide temporary protection from creditors. This may be something that could be offered after discussions with a debt adviser. When in place, your creditors won’t be able to contact you about your debts or add interest or charges while you make repayments, for a minimum of 30 days.”

You can also receive free and confidential support and advice from Debt Advice Foundation or StepChange.

The article above includes general information and should not be taken as financial advice. If you have questions about your specific circumstances, please speak to an independent financial advisor.

If you haven’t already, why not try our free Budget Planner? It only takes around 10 minutes and it’s available for everyone – not just Starling customers.

Try our Budget Planner