Your Business Marketplace

Choose from a range of smart integrations that allow you to connect your Starling app with all your favourite products and services, from your accountancy software to your payments platform.

Marketplace only has a fraction of the financial products available on the wider market. We receive commissions or a referral fee from some of the products we feature, but this would have no impact on the cost to you.

To make sure you choose a product that suits you best, do your own research to find out what else is out there before making a decision.

How our

integrations work

Tailored to your business.

As no two businesses are the same, we’ve curated a wide range of integrations, so you can select the ones that are just right for you.

Open banking.

Our integrations are made possible by Application Programming Interfaces (APIs). These let you share your data securely with trusted providers in real time.

Get more from your banking app.

Use your Starling account for more than just banking. From never having to manually upload bank statements again, to keeping track of your insurance renewal dates.

Secure.

All providers listed in the Marketplace are vetted and they can only access the personal information and transaction data you consent to sharing.

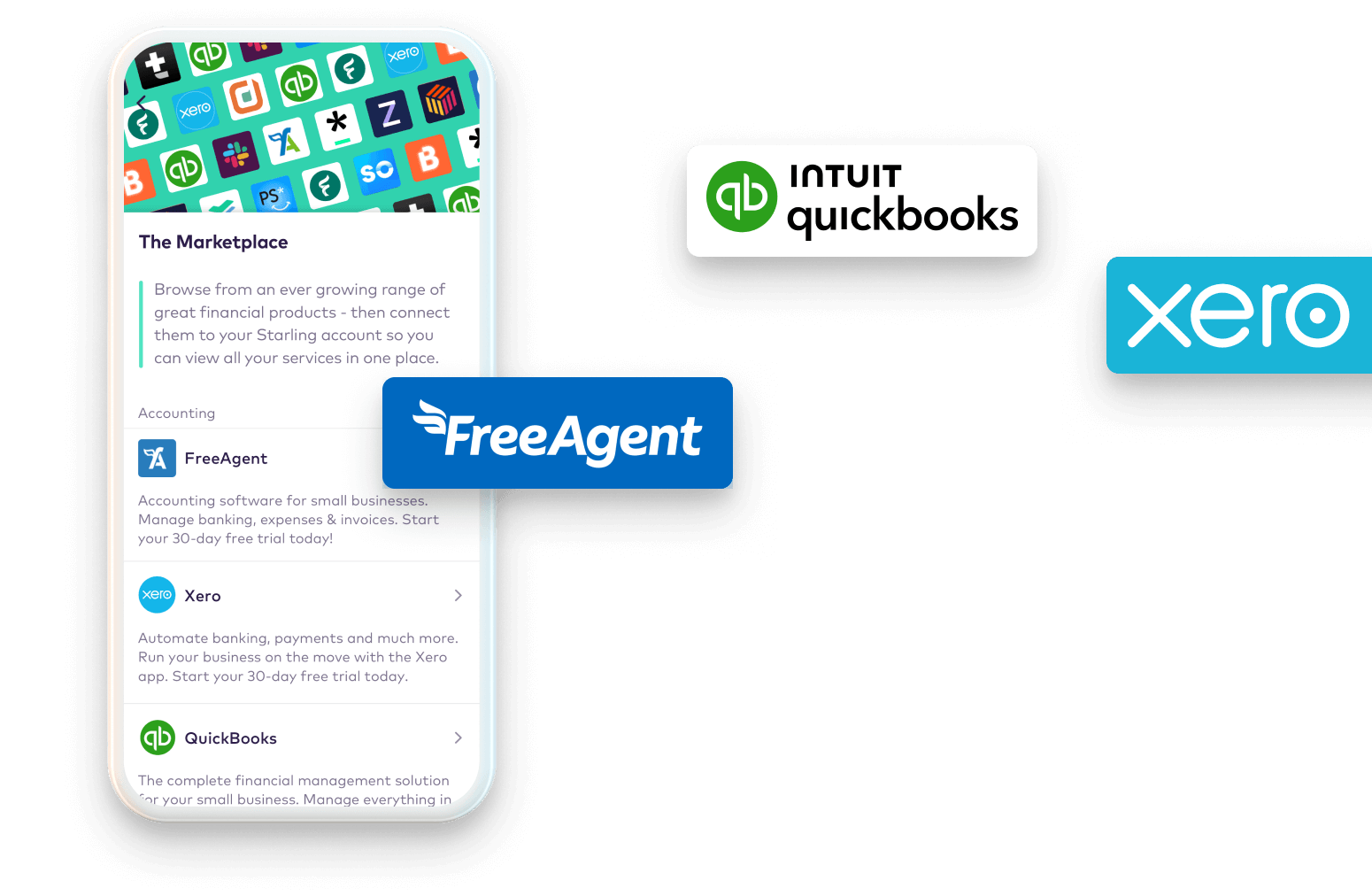

Accounting

Share all your banking data with your accounting software, automatically and in real time.

Automated: transactions on your Starling account are shared in real time with your accounting software, saving you time on bookkeeping and reducing the chance of any errors.

No fees: If you’re signed up to Xero, QuickBooks or FreeAgent, you can access them from Starling’s fee-free business bank account.

Starling currently supports integrations with Xero, QuickBooks and FreeAgent. If you don’t see your accounting software provider in our Starling Marketplace (e.g. Clear Books, Crunch, KashFlow), there’s a good chance you can still sync your Starling account via their platform as they may have built a connection to us directly.

Prefer built-in tools instead? If you’d rather keep everything under one roof, Starling Accounting lets you manage your banking, bookkeeping and tax all in one place – no extra integrations needed. Learn more about Starling Accounting.

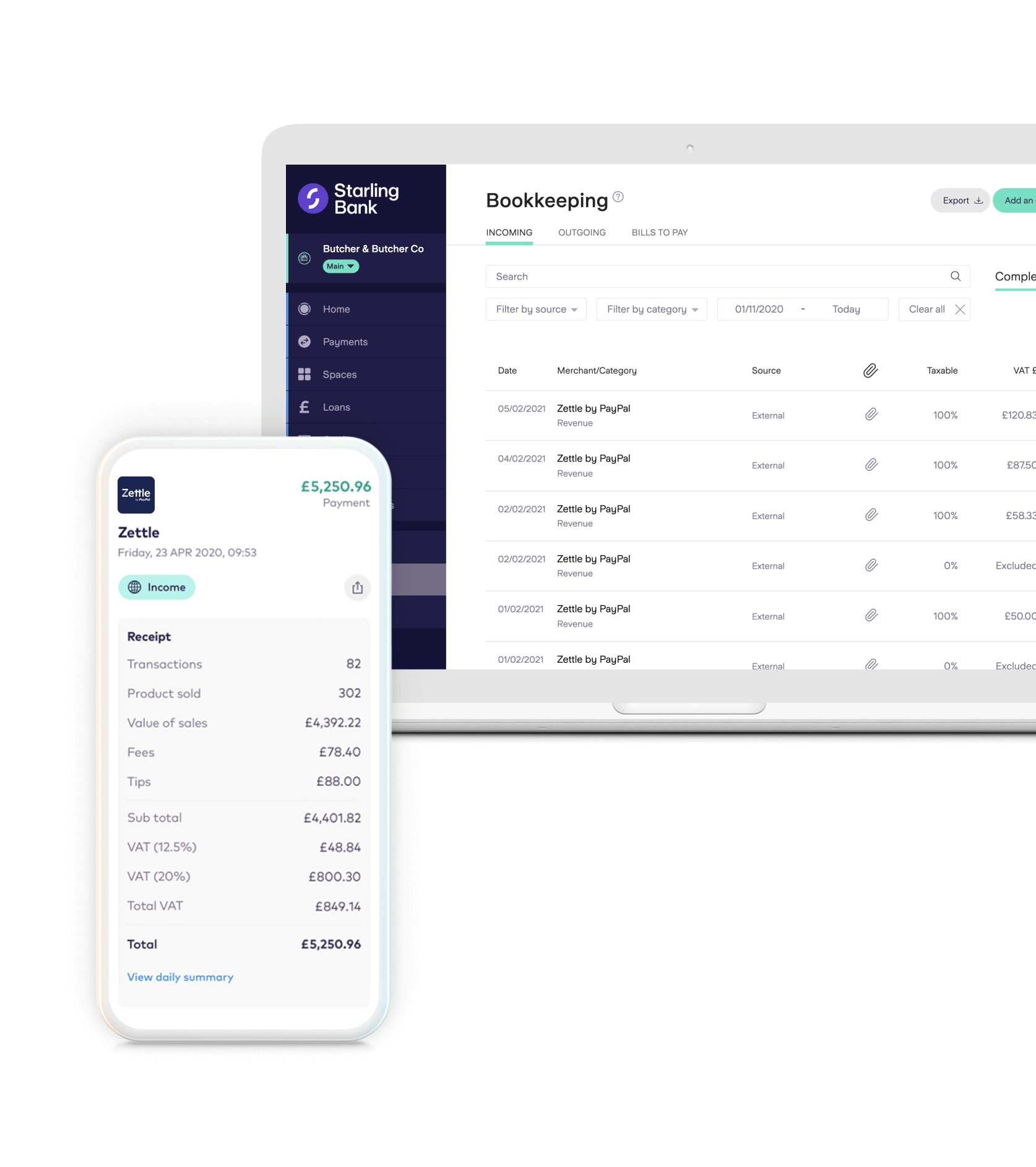

Payments

Link your Starling app to leading point-of-sale platforms Zettle and SumUp. You can receive detailed summaries on all your incoming payouts, including transactions, fees and VAT.

Get the benefits of linking your banking with your payments

Insightful: get richer data on your payouts and track high-level performance data.

Seamless: easily navigate between accounts.

Business integrations currently available

Categories

Get more out of Starling

Already got a business account? Apply for a personal account in just a few taps.

Find out moreThe Starling Promise

We don’t have any hidden markups, so you’ll pay the same as you would by going direct to the provider. It’s what we call the Starling Promise.

Apply for a business account today and enjoy app-based banking at its best.

Start your applicationAlready a Starling customer? No need to download anything new - you can browse the Marketplace in-app. From the home screen, tap the top right icon, then tap ‘Marketplace’. From there you can explore all of our integrations.