Standing orders and Direct Debits are automatic payment methods that are used to make recurring payments.

Direct Debits

What is a Direct Debit?

A Direct Debit is an instruction given to your bank that gives permission to a business to take payments from your account. The business can make changes to the payment, however they will need to let you know you first.

Payments made by Direct Debit are protected by the Direct Debit Guarantee. This means that if there is a payment error, for example, if the payment is taken on the wrong date or an incorrect amount is taken, you will be refunded.

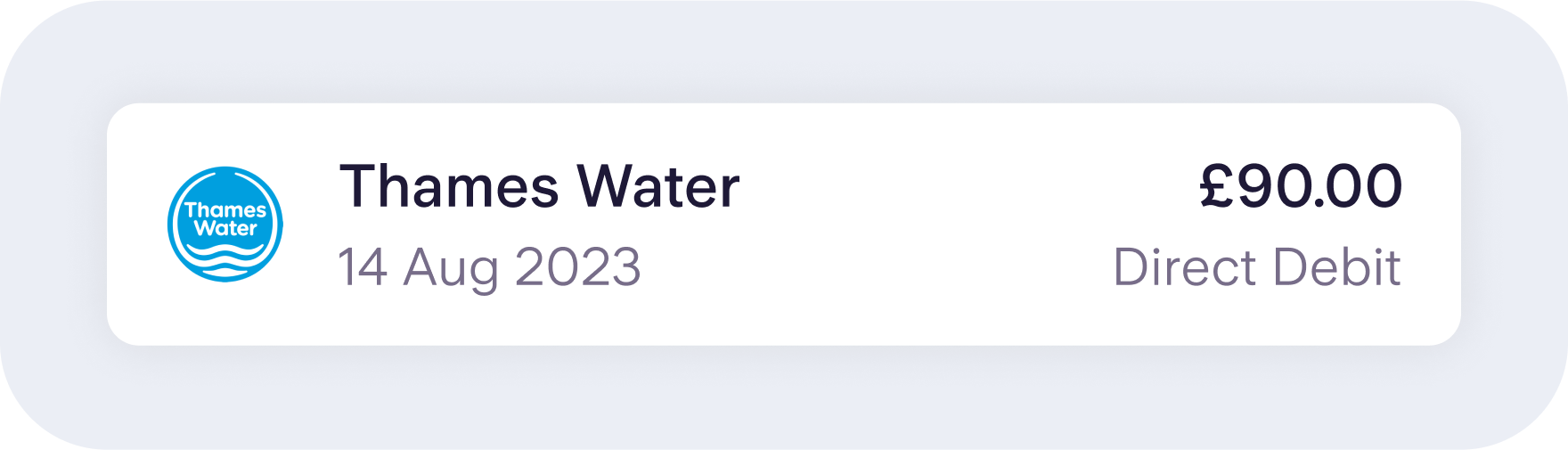

Direct Debits are often used for regular utility bills, such as energy and gas or subscriptions, such as gym memberships and streaming services.

With Starling’s Bills Manager feature, you can pay Direct Debits and standing orders straight from a separate Space – they’ll be automatically paid on their scheduled date.

How do Direct Debits work?

When setting up a Direct Debit, you give permission for a business to automatically take payments from your bank account on a specified date. You can usually choose the date when the Direct Debit will be taken.

How to set up a Direct Debit

Direct Debits are set up by businesses and serve as an easy and efficient way to collect regular payments from customers through an agreement called a ‘Direct Debit Instruction’.

To set up a Direct Debit, you’ll need to provide the business or organisation with your bank account details. This can include:

the name and address of your bank or building society

Normally, the business gives you a form to fill in and send back to them. Once completed, the organisation will send your instructions to your bank, giving them permission to take money from your bank account.

You can usually set up Direct Debits over the phone, online or in-app.

How to cancel a Direct Debit

You can cancel a Direct Debit at any time. To cancel, contact your bank or building society. Some banks let you cancel through online banking or in your mobile banking app. You can also cancel a Direct Debit on the phone or by writing to your bank. It’s also recommended to notify the business involved that you wish to cancel the Direct Debit.

Advantages and disadvantages of Direct Debits

What are the advantages of Direct Debits?

Convenient and saves time as you don’t need to remember to pay every month.

They can be cancelled at any time.

In the event that an incorrect payment is taken, you will be refunded.

Are there any disadvantages?

Direct Debits get rejected if there isn’t enough money in the account. Make sure you always have enough for the next billing cycle.

Companies can change your payment dates and amount of money to be taken. However, they’re required to let you know in advance if there are any changes.

Try our award-winning current account

Get more from your money with Starling’s simple, award-winning current account. With features such as instant notifications, Spending Insights and Spaces, money management has never been easier. Apply in minutes from your phone.

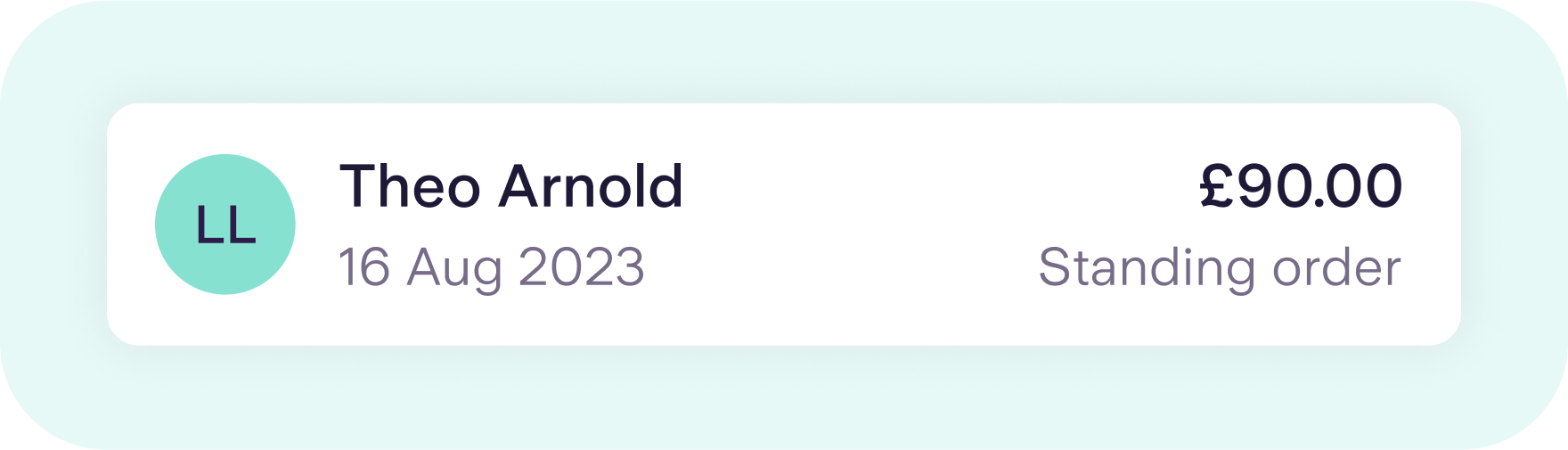

A standing order is a recurring payment that allows your bank to take a fixed amount of money from your account on a specified date at regular intervals.

Standing orders are normally used to pay bills (such as electricity, internet, or subscriptions), rent or mortgage instalments, and for regular transfers to other accounts, such as friends and family.

Standing orders can be changed or cancelled at any time.

How to set up a standing order

Standing orders are often easy to set up through your online banking or mobile banking app. If your bank has branches, you can do this in person or over the phone.

When setting up a standing order, you will need:

the recipient’s bank details (sort code and account number)

amount of money to be transferred

payment frequency e.g. monthly, yearly

payment reference

Advantages and disadvantages of a standing order

What are the advantages of standing orders?

Easy to set up and cancel.

Useful for fixed and recurring payments.

You’re in control of setting the amount of money, frequency, and how long it should be set up for.

Are there any disadvantages?

If they aren’t set up in time, you can miss the payment date and could incur late fees.

If the amount or date changes, you will need to cancel the standing order and create a new one.

Higher admin time, especially for businesses. Business owners may have to regularly check that payments have been made and received.

What happens if a standing order is not paid?

Mostly, this happens because you don’t have enough money in your account. If the standing order payment fails, you’ll need to make a separate one-off payment as it won’t be taken automatically from your bank account after the missed fixed date.

How long do standing orders take to clear?

Standing orders are usually processed the same day they are set up. However, you should allow 3-5 working days for the money to reach the recipient’s account.

If your standing order is due to be paid on the weekend (Saturday/Sunday) or on a bank holiday, the payment might not be received until the next working day.

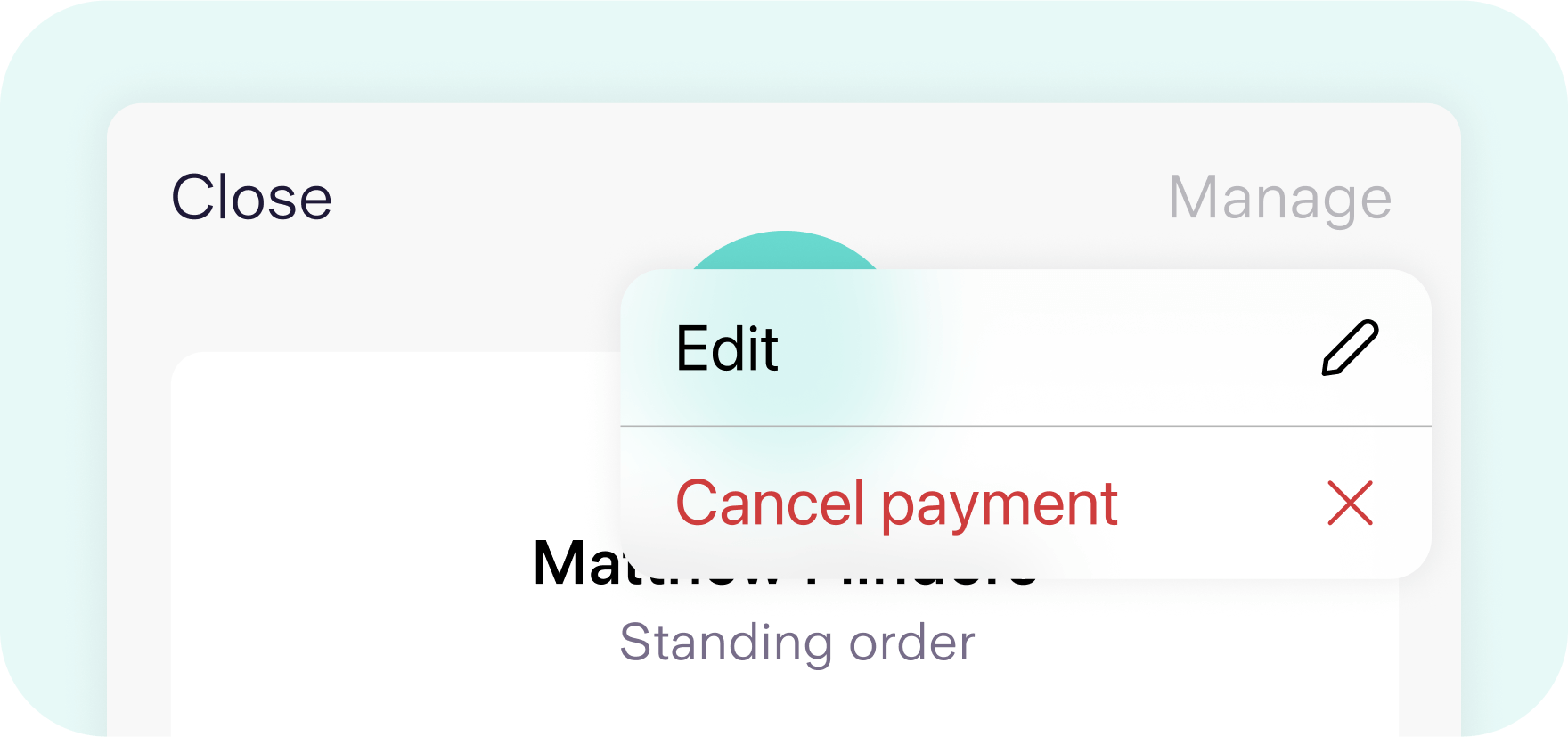

How to cancel a standing order?

If you want to stop or change a standing order, you’ll need to cancel it.

Many banks offer the option to cancel a standing order through your online banking or mobile banking app. It can also be done on the phone or in-branch (if your bank has branches).

Each bank has their own processing time for cancelling standing orders. Usually, if you cancel your standing order online two days before it’s due, the payment will not go through.

What is the difference between standing orders and Direct Debits?

The main difference is who controls the payment. With Direct Debits, you give a company permission to take money from your account on an agreed date. With standing orders, on the other hand, you tell your bank to transfer money from your account on a fixed date.

Another difference is the payment amount. With standing orders, the amount is the same every month, but Direct Debits can change.