Fighting fraud

How to protect yourself from APP fraud

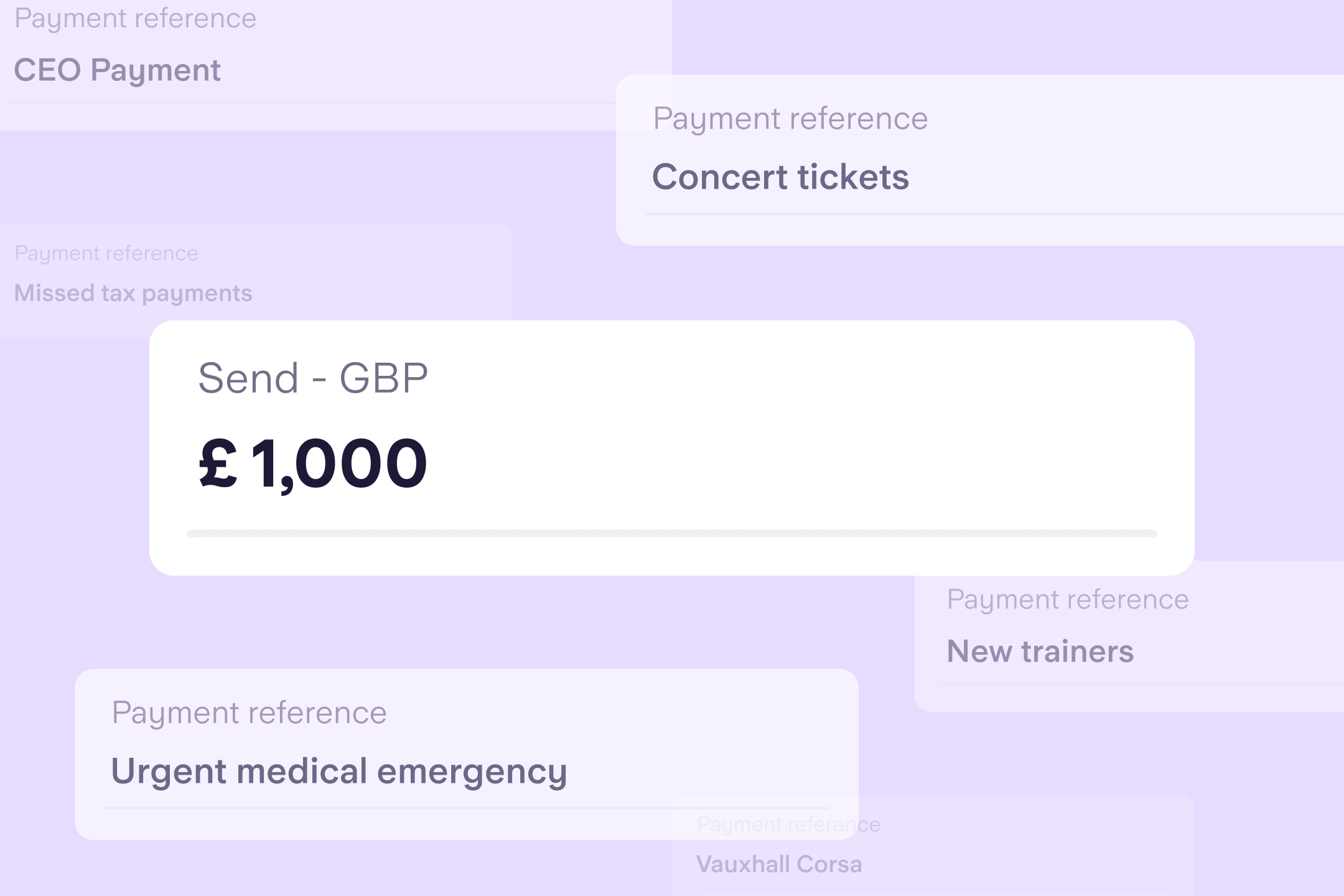

When a criminal tricks someone into willingly making a bank transfer to them, this is known as APP (Authorised Push Payment) fraud. Learn how to protect yourself.

By Starling Financial Crime Specialist