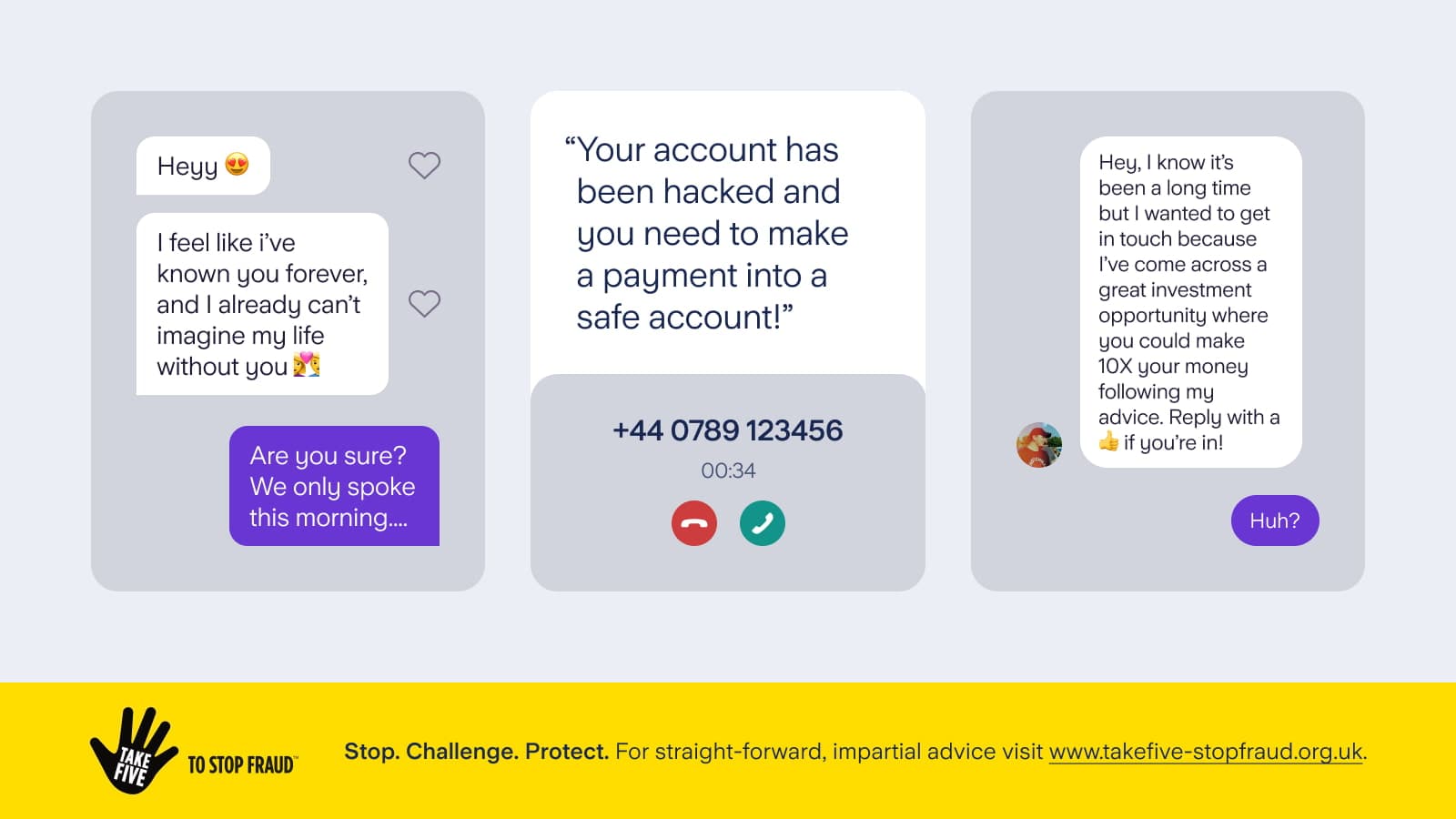

Personal finance

“We couldn’t get on the pitch – there were loads of men playing. The girls were so disappointed.”

15th May 2024

Credit scores are one of the many things we only seem to come across in adult life. And one of the many things that can add to the feeling of frustration that money wasn’t covered enough in school.

Here, we offer an explanation and go through what you could do to help improve your credit score while renting a flat or house.

A credit score is a number that represents how reliable the credit reference agencies think you are when it comes to paying back debt. For example, a high credit score could indicate that you have shown that you’ve made mortgage or loan repayments on time, without missing repayments.

On the flipside, a low credit score could reflect that you either haven’t got a history of paying back any debt or haven’t stuck to the terms of a loan, mortgage or credit arrangement, for example by missing credit card repayments. Other factors that can negatively influence your credit score are being close to your credit card or overdraft limit and applying for credit from multiple companies in a short space of time.

Your credit score is usually different for each credit reference agency, as they each have their own system and way of showing you how you’re performing. The main credit reference agencies are Experian, Equifax and TransUnion.

Experian, which gives you a credit score out of 999, considers a good credit score to be anything above 880. While Equifax gives you a score out of 1000 and considers a very good credit score to be more than 670. For TransUnion, your score will be out of 710. It considers a score above 603 to be ‘very good’ and a score above 627 to be ‘excellent’.

Your credit score matters because it can impact how much you can borrow, for example through a mortgage or a personal loan. It can also be a factor if you want to buy a car on finance or if you want to buy a new smartphone through a pay-monthly contract. Ultimately, your credit score matters because it can help you reach a financial goal.

If you’re renting but hoping to secure a mortgage, you can sometimes feel like you’re in a bit of a catch-22. You usually need a good credit score to be offered a mortgage with a good rate, but in order to build a good credit score, you often need to show a reliable record of making repayments of some kind. But you may not have had many such repayments to make if you haven’t had an overdraft, credit card, loan agreement or mortgage.

This ‘catch-22’ is a challenge that CreditLadder, one of our Marketplace partners, aims to solve (Starling’s Marketplace is where customers can connect to third-party apps and services, straight from the Starling app). CreditLadder enables you to register your rent payments with the main credit reference agencies to help you improve your credit score. It does this through gaining your permission to ‘read’ your rent payments when they’re made from your bank account to your landlord or agent.

“Rent payments started to be registered when they came out of my Starling account,” says Jo, a Starling customer who used CreditLadder for two years to improve her credit score. “My credit score went from ‘poor’ to ‘good’ in the time I used it - I didn’t think ‘good’ was great but it was enough for me to be able to get my mortgage, which I applied for with my partner.” Jo, 30, and her partner bought their property in Edinburgh.* In the section below on What else can I do to improve my credit score, we explore many of the other things you can do to try and improve your credit score.

If you want to try out CreditLadder, you can find out more by going to the Starling Marketplace.

“The process of signing up in the Marketplace was very straightforward,” says Jo. “Recording something you’re already doing anyway, like paying rent, is a no brainer. It shows you’re responsible and shows that you can pay what you owe on time.”

Dion, 25, who bought his property in Manchester, also used CreditLadder to improve his credit score. “When you sign up, you specify whether you want to use the free service, which reports your rent payment to one credit reference agency (Experian, Equifax or TransUnion), or you can pay £8 a month [correct price at the time of publication] and they’ll report it to all of them. You then specify the date your rent is supposed to come out and then when the payment is made, it's registered with your chosen credit reference agency. It was a really simple thing to set up to improve my credit score before applying for a mortgage.”

If the amount you pay in rent changes or you’ve arranged a rent break with your landlord or agent, it’s important to let CreditLadder know as soon as you can. This is because, once you've signed up to CreditLadder, a late or missed rent payment could negatively impact your credit score.

One easy step to take to try and boost your credit score is to register on the electoral roll at your current home address. This will help credit reference agencies and lenders confirm where you live and who you are.

If you have a credit card or a loan, one of the things you can do to demonstrate your creditworthiness to credit reference agencies is making repayments in full and on time.

There are also several things you can avoid doing to make sure you don’t lower or damage your credit score. For example, you should avoid making too many credit applications in a short space of time. Maxing out your credit card or overdraft limit is also something to avoid, as it will look as though you’re too reliant on credit or your overdraft.

It’s important to pay your utility bills and mobile phone bills on time and in full and to keep up with any repayments on a credit card, loan, mortgage, or for any other credit arrangement you have in place. Paying by Direct Debit can help with this. That said, missed repayments could be recorded on your credit report for up to six years, so make sure you have enough in your account to cover repayments made by Direct Debit. If you’re a Starling customer, we’ll send you notifications for upcoming Direct Debits to help you keep you on top of these.

“Starling truly makes everything so easy,” says Jo. “It makes me feel so safe and secure.”

*Each lender has their own lending criteria. The steps you take to improve your credit score may have a different impact, depending on the lender.

The above article is intended as general information and does not constitute advice in any way. You should take independent advice if you have any questions about your specific circumstances. For advice, a good source of free information is Money Helper, an independent organisation backed by the government.

Personal finance

15th May 2024

Personal finance

13th May 2024

Personal finance

7th March 2024

Money Truths

2nd July 2025

Money Truths

1st July 2025

Money Truths

29th May 2025